Noble Group (來寶集團) has no or few audited flow supporting their 48B$ sales of commodities.

According to the industry, their turnover, by any account, would appear as vastly overstated.

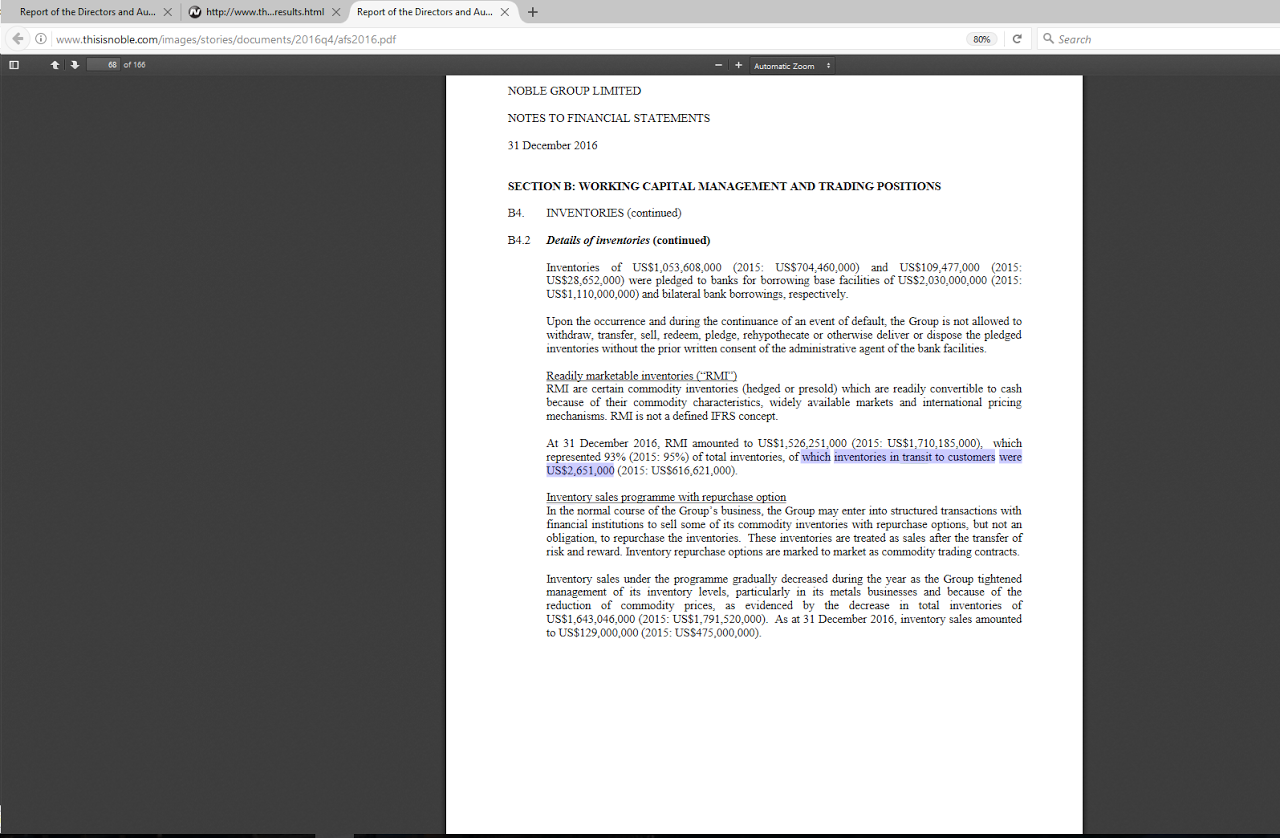

Noble Group Ltd. Financial Statements 31 December 2016

As of May 2017 the company had YTD losses (330) Millions in operating cash-flows but self-assessed itself with a net equity of $3.849B while of this net equity is tied to the fair value gains of its derivative and long-term commodity contracts.

Iceberg Research, the research firm has challenged Noble Group (來寶集團) over mark-to-market accounting of these contracts.

Bankers know that the last 24 months have been punctuated by a series of catastrophes, credit downgrades and bizarre resignations at Noble.

CEO ex-GS Alireza, Mr. Elman and Noble Group’s chief financial officer Robert van der Zalmin in particular who has stepped down from his position after taking a leave of absence for “health reasons”.

Traders (smart money) have also left at the right time. (Fabrizio,Steve Bader, Paolo B, Ted, Doug M..)

As of Q1-2017, Noble Group (來寶集團) had $3,4B of marked-to-market fair-value gains on derivatives and commodity contracts.

What does the $3.4B MtM figure represents ?-this MtM is not contracts that can be liquidated to cash.

Mark-to-market (M-t-M)

To mark-to-market is to calculate the value of a financial instrument (or portfolio of such instruments) at current market rates or prices of the underlying.

Example for illustrative purpose:

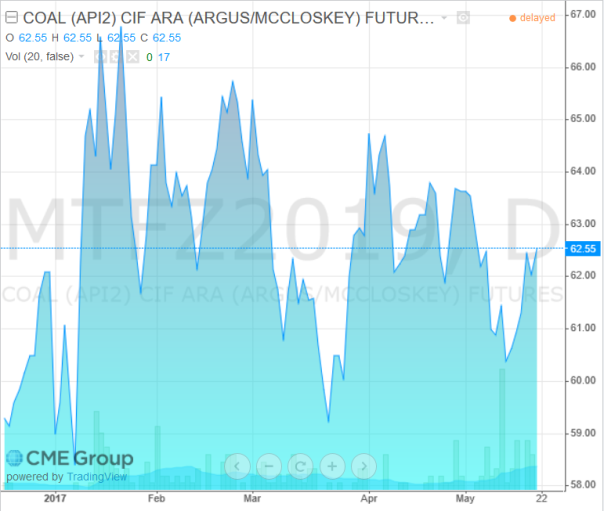

On 1 Jan 2017: Noble buys 2,000,000 MT for June 2019 delivery at $59/mt. It turns immediatly in the derivatives market and sells the equivalent of 2,000,000 MT of paper contracts. This is the Coal API2 Argus futures contracts.

This is the Coal API2 Argus Futures Contracts.

Timeline

1 Jan 2017: Noble has a +MtM of 0 (Contract price is $59 and the Argus Futures is at $59)

1 Feb 2017: The Argus Coal API2 futures is at $64,25. The +MtM on the coal contract is +$10,5M

20 March 2017: The Argus API2 Futures dropped to $59,25/MT The +MtM on the coal contract is +$500K

1 May 2017: The Argus API2 settled at 62,55 and the +MtM on the coal contract is now +$7,1M

–

Noble Group MtM on Coal contract:

–

The 2,000,000 MT of Coal produces a MtM gains between $500K and $11.5 millions.

Capezize Ship

In order to produce $3.4B of MtM gains one would have to buy not 2,000,000 MT of coal , as in this example, but nearly 958 million metric tons – the equivalent of 6937 Capezize cargoes Richards Bay-Qingdao, China or 5 voyages per week for the next 13 years… plus an equivalent position in the derivatives.

This represents a considerable tonnage even for the largest firms of the industry (Cargill, Rio Tinto, BHP, Vale, Anglo American) put all together.

According to BP statistical review of word energy 2016, the world coal production was 786.1 million tonnes (2015)…

An inevitable conclusion is that Noble uses a mountain of derivatives to maintain its MtM coal pile or … something else

Back-of-the-envelope calculations suggest that the $3.4B MtM mark used by Noble Group(來寶集團) translates to coal hedges at 479 USD/MT– The Argus APi2 CIF Rotterdam futures in the $60s/mt.

So…. Accounting fraud …. ?

Won’t be the first time…

These days Noble is looking to refinance a $3.849B net equity. which has more the financial substance of a “Fair-value to-arrive equity” (sic)

This happens at a moment when Noble has just screwed up both its recent fixed income investors and shareholders.

The thing that frightens banks the most is not having a good risk management process in place because it opens the possibility of financial losses and frauds. A trader with no risk management is like playing roulette; double or quits.

Fraud is the worst nightmare for any bank specialized in commodity lending, but some will always chasing the“tails” in Hong Kong no matter what.