Last year we predicate that refinancing Noble (來寶集團) would be a lose-lose deal in which everyone would end up looking bad.

“At some points the Banks must get out, must unload the RCF risk with the red pill and it means that Noble will work for the Banks”.

“This is the equity offering of a company with very questionable or no prospects, transferring risks to retail investors”.

In short, this is a lose-lose deal in which everyone ends up looking bad”.

Refinancing Noble: a Lose-Lose Deal

The only thing we got wrong in 2016 is that some Banks would still accept to refinance the liabilities of Noble (來寶集團) on the back of an equity raising.

The investors have eaten the red poison pill and we simply overestimated their level of sophistication.

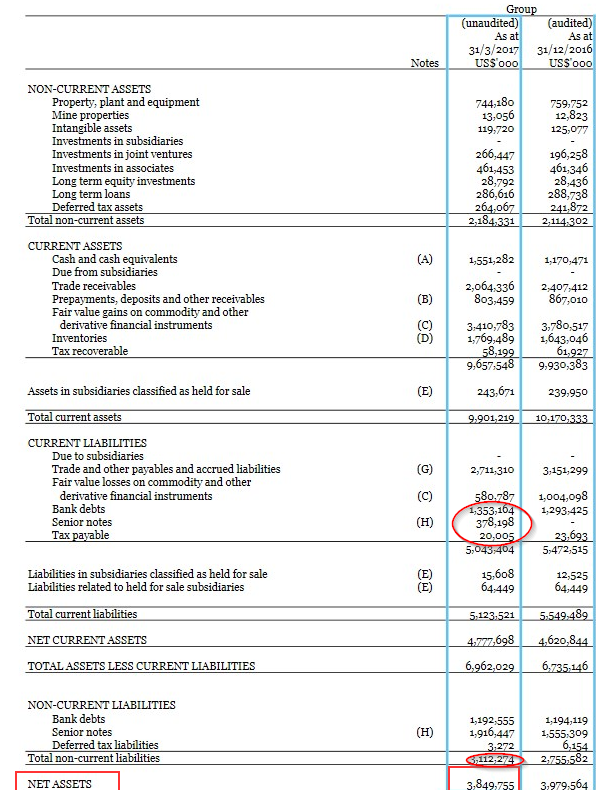

Can anybody look back and say it was good to let Noble raise more than 1.2B in equity offering and bonds ?

- The 750M bond raised is traded at 40c on the dollar.

- Equity investors who also subscribed to the 500M share rights issue at 0.20/share are now at 0.03…

Success can’t be imposed on this circus.

Given that the Operating loss is created by a mismatch between the level of profits booked on these derivatives and commodity contracts and their underlying expected cash-flows, the real nature of this MtM can be viewed as an expensive liability that Noble (來寶集團) has to roll-out.

Noble (來寶集團) has even pushed back against guidelines in Singapore for disclosing information on its executives’ remuneration.

Perhaps Noble (來寶集團) needs to raise another 2B to pay coming debt retirement (reassure the lenders that they refinance the fair to arrive net equity on a future solvency basis) – as the book doesn’t generate positive cash-flow since 44 months.

It is no longer a working capital shortfall that we observe but the liquidation of a trader (virtually silent in the physical market)…

Lenders will choose to roll up credit. IF not, they precipitate a restucturing which is told to be not in the interest of the 2020 and 2018 bond holders (FT).

It should be pretty clear.

This time Noble (來寶集團) will work for itself, not for the banks.

On the road show, Noble has asked the permission to decrease its net equity.

It wants to set its own “term sheet” and its covenants to be relaxed, exactly the opposite wanted by the other side.

4 Banks are long with a $1.5B exposure left with this intermediate situation :

- no financial substance.

- no unencumbered assets.

- no physical trading traceability.

- A porous risk management and a total absence of management oversight.